For sports fans the past two weeks have been nirvana with Olympics 2020 in Japan not to mention our own hurling equivalent, Formula 1 drama etc. It is hard to beat watching such dramatic sporting events particularly when a small nation like ours delivers such lovely winners like Kellie Harrington. One common theme that runs through every event is how fit and healthy the participants are and their enthusiasm for doing something they are passionate about. Thankfully they are far removed from illness and long may that always be the case.

Unfortunately for many of us, the reality is that fitness and health are far below ‘Olympic’ standards and this is a trend that shows no sign of abating in Ireland. Our aging population and unhealthy lifestyle habits are contributing to the country's rising cancer rate. Ireland has the third highest cancer rate in the world, according to a report from the International Agency for Research on Cancer, part of the World Health Organization (WHO)*.

*Sept 2018

This is one of many frightening stats that should make us all sit up and take notice even at a time when the world and our media are obsessed with another dirty C word namely ‘coronavirus’. To put it bluntly

We are facing a future where one in two of us will get cancer

Source: Averil Power, CEO of the Irish Cancer Society in April 2019

Not to mention…

One in three men and one in four women will get an invasive cancer before the age of 75!

Source: Cancer in Ireland – Annual Report of the National Cancer Registry

Frankly there are so many alarming stats that one nearly becomes numb to it all and I suspect it is this ‘numbness’ that contributes to the inertia amongst us towards getting insurance cover for such a horrible illness. Yet as Zurich’s recent 2020 claims show – cancer is the biggest factor behind deaths and serious illness in Ireland.

Cancer & heart related deaths accounted for 67% of all death claims in 2020

Cancer accounted for 67% of all Serious illness claims in 2020.

63% of all male claims were related to cancer.

74% of all female claims were related to cancer.

Sadly, many of us have lost loved ones to cancer and very few Irish families have escaped the damage it causes not just in human and emotional terms but also in financial terms. A 2015 report by the IrishCancer Society highlighted the severe financial implications that typically arise:

Increased medical costs such as consultant fees and expensive medications.

Actual out of pocket expenses such as increased travel to appointments that may be in medical centres of excellence located a distance away from home.

Increased utility bills due to the extra time spent at home recovering from surgery.

Reduction in earnings due to patients (and their family members) having to take time off work. This is particularly relevant for those that are self-employed.

The report also put in an estimated figure which was €2,600 per month – that was what cancer can cost a patient. Bear in mind that this report was 6 years ago and we all know that in Ireland …costs only go one way!

In an ideal world it would be cover that is as prevalent as mortgage protection but the latter is mandatory as you need it to cover your bank’s ass. In reality, you really need cancer cover to cover you and your family’s posterior and more, particularly if you are beginning to get a few grey hairs.

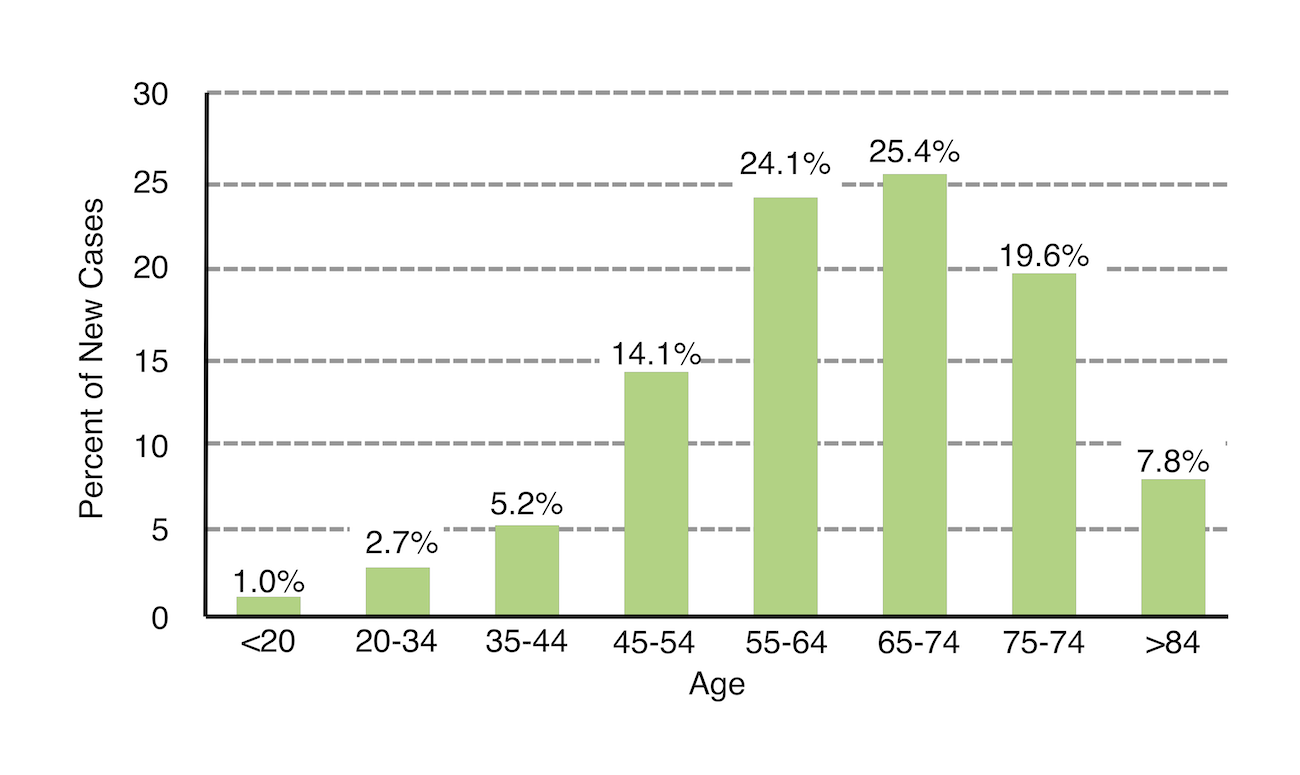

This isn’t a surprise because as we get older the odds of us getting cancer also rise considerably so it’s a policy you really need to get before ‘sniper alley ‘kicks in which is between the ages of 55 – 75.

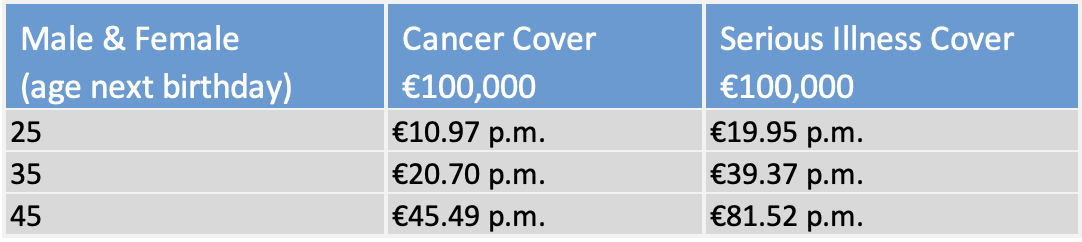

Now down to the ‘nuts and bolts of how to get cancer cover and what it involves.

Cancer cover is a policy that pays a lump sum on diagnosis of Cancer (as defined in the policy document)

It is cover that is relatively recent with Zurich Life the only provider that offers it in the Irish market. Up to its launch, the only way a person could get cancer cover was via a typical serious illness policy. This was all well and good but serious illness cover...

(a) is typically expensive ..plus

(b) underwriters can be quite tough in terms of deciding if they will underwrite you for this type of cover or not.

Cancer cover neatly steps over these obstacles as it can be provided to an individual who would ordinarily be declined full Serious Illness Cover. This includes people with a medical history of:

Heart Attacks

Angioplasty

Angina

Valvular Disease

Stroke

Obesity

Diabetes

Kidney Problems

It also costs much less which is very beneficial where one’s budget cannot stretch far enough to purchase full serious illness cover.

In addition, Cancer Cover can also be added to other cover in the same way as serious illness cover is and this is a very good way of adding another crucial layer of protection at a relatively small cost. For as little as €10 per month one might be able to put in place a significant amount of cancer cover.

This is not the type of blog one should ideally be reading on a carefree Summer’s holiday in the lazy hazy (rainy!) days of August but the flipside is that sometimes these are the only days where one can sit back (or down) and really ‘see the woods from the trees’.